The Most Powerful Players in Insurance Are the Ones You’ve Never Heard Of

Insurance power doesn’t sit with the companies you see, it sits upstream with reinsurers who control capacity and dictate what the market…

Insurance power doesn’t sit with the companies you see, it sits upstream with reinsurers who control capacity and dictate what the market can do.

Re is building at that leverage point, opening the reinsurance layer that underpins real global economic activity to onchain capital:

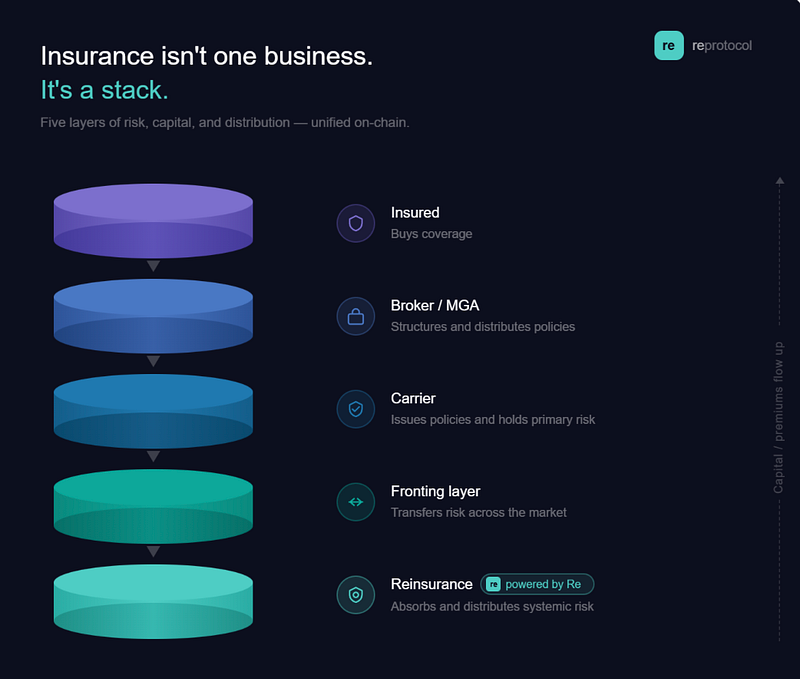

- Insurance is essential to functioning markets and global activity. Behind it is a stack of players, each with a different role and a different level of influence.

- Reinsurers sit upstream from insurers and quietly shape what the entire market can do, which risks get covered, at what scale, and on what terms.

Re is building in the reinsurance layer, the part of the stack where structural leverage actually lives.

Insurance Is a Stack, and Power Lives Upstream

Most people think insurance is simple: you pay a premium, a company takes on your risk, and when something goes wrong, they pay out. The company you call, argue with, and renew with every year feels like the center of the system.

It isn’t.

Insurance is a stack. Without it, capitalism and markets can’t function. Homes can’t be bought and sold, goods can’t be shipped across oceans, and growth is hampered.

Between you and the capital that ultimately backs your policy, there are five distinct layers: brokers, MGAs, carriers, reinsurers, and the capital providers behind them.

But they don’t have equal leverage. And the layer with the most structural power is the one furthest from the customer: reinsurance, who provide the capacity that determines what risks can be written, at what scale, and on what terms.

Each layer plays a role, but the deeper you go, the more influence there is over how the market actually functions.

Reinsurers set the constraints everyone else operates within.

Reinsurance is insurance for insurance companies. When reinsurers supply capacity freely, insurers write more, price competitively, and expand coverage. When they pull back, everything downstream adjusts, whether the downstream players want it to or not.

Consider what happened in the U.S. property insurance market in recent years. As climate related losses mounted, reinsurers began pulling back from catastrophe exposed regions. They raised prices, tightened terms, and in some cases, stopped offering capacity in certain regions.

Carriers who could no longer reinsure their Florida books stopped writing new policies. MGAs who had built wildfire products around reinsurance treaties saw those treaties non-renewed. Brokers couldn’t find markets for their clients. Homeowners found themselves with far fewer options, and in some cases, no private coverage available at all.

The reinsurers didn’t make any of those individual decisions. The carriers, MGAs, and brokers each made their own choices under their own pressures. But the upstream withdrawal of reinsurance capacity is what made all of those downstream decisions inevitable.

That’s the nature of structural power: it shapes the terrain that everyone else navigates.

The players closest to the customer are the most visible. They field the calls, take the blame, and build the brand. But visibility is not the same as power. The further you go from the customer, the closer you get to the structural forces that determine what the market can actually do.

The Foundational Layer Where Re is Building.

DeFi has spent years rethinking who gets to be a lender, a market maker, a liquidity provider. Re applies the same logic to reinsurance, opening up the layer that has historically been the most consequential and the most closed.

Re operates directly in the capacity layer: the part of the stack that determines what the entire market below it can or cannot do.

This is the problem Re is built to solve. Through Re, onchain capital can back real insurance programs, earn underwriting premiums, and participate in the upstream layer where insurance economics are actually set.

If you want to understand insurance, you have to look past the insurer. The real leverage is upstream. It always has been, and that’s exactly where Re is building.

Re is building where the leverage actually lives.