How Losses Flow at Re: Understanding the Senior & Junior Capital Structure

Re is turning underwriting into a capital stack backed by real-world insurance premiums. Here’s how reUSD, reUSDe, and Re’s capital layer…

Re is turning underwriting into a capital stack backed by real-world insurance premiums. Here’s how reUSD, reUSDe, and Re’s capital layer were designed for predictable outcomes under extreme conditions.

Key Points

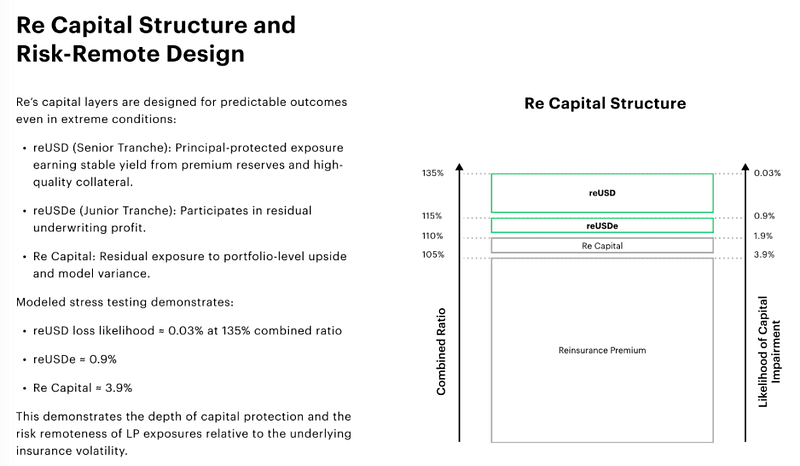

- A 135% combined ratio, historically about a 0.03% probability event, would be required before losses could reach token holders, compared with Re’s current 92% combined ratio.

- The capital stack is structured so losses flow sequentially through premium income, retained reserves, reUSDe (junior tranche), and finally reUSD (senior tranche).

- This structure gives the tokens distinct risk profiles: reUSDe sits closer to underwriting results and earns higher yield with more exposure to volatility.

- reUSD sits behind multiple layers of protection as the senior tranche, meaning an extreme and historically rare loss scenario would need to occur before it is ever impacted.

Resilience by Design

Reinsurance underwriting produces predictable outcomes over long periods, but any capital structure built on underwriting must be transparent about how losses are absorbed. Re’s capital stack is designed to make that process explicit: Premiums flow in from diversified reinsurance portfolios, losses are absorbed in a defined order, and different capital layers participate in underwriting performance differently.

The structure similarly to senior and junior tranching in structured finance. Each layer carries a different level of exposure to underwriting volatility, and earns a different level of return.

Overview: Re’s Capital Structure

The structure flows in four layers. Understanding how losses move through that structure is the key to understanding both reUSD and reUSDe.

- Premiums → absorbed first

- Retained capital and reserves → grows with every profitable year

- reUSDe (junior tranche) → closer to underwriting performance

- reUSD (senior tranche) → protected by all above it

The diagram below illustrates how these layers sit within the capital stack.

Reinsurance Premium: What Combined Ratio Means

Insurance and reinsurance performance is typically measured using a metric called the combined ratio. In simple terms, the combined ratio measures how much insurers pay out relative to the premiums they collect. It is calculated as claims plus expenses divided by premiums.

When the combined ratio is below 100%, underwriting is profitable, i.e. premiums exceed the total cost of claims and operating expenses. When the combined ratio is above 100%, underwriting generates a loss.

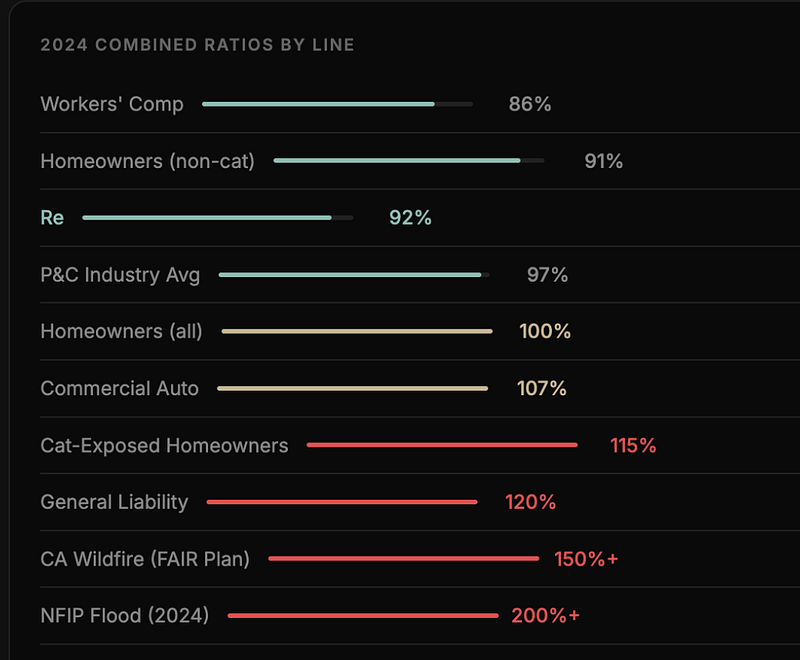

For many diversified insurance lines, underwriting results tend to cluster comfortably below 100% over time. Workers’ compensation insurance, for example, has historically produced combined ratios around 86%. Diversified commercial insurance lines often run between roughly 90–93%.

Re has produced a combined ratio near 92% across cycles. In contrast, catastrophe heavy lines such as hurricane, flood, or wildfire insurance can produce combined ratios well above 150% in severe disaster years, because a single event can generate large losses across an entire region.

Re’s underwriting strategy avoids that type of concentrated severity exposure. Instead, it focuses on diversified, frequency driven insurance lines where many smaller claims occur across different geographies and policyholders. Over time, that diversification helps stabilize underwriting results.

What Happens in a Typical Year

At a 92% combined ratio, Re operates profitably: premium income exceeds claims and expenses. In these conditions, losses never move into the capital stack and all protection layers remain untouched.

Instead, surplus accumulates as retained capital and reserves on Re’s balance sheet, strengthening the first-loss layer within the capital structure.

Over time, profitable underwriting years compound this buffer. As retained capital grows, future losses would need to pass through an increasingly larger layer of protection before ever reaching the junior or senior tranches.

In practical terms, this means reUSDe and reUSD holders remain fully protected, with safety margins expanding as underwriting profits accumulate.

What Happens in a Stress Year

If claims and expenses exceed premiums in a stress year, the combined ratio rises above 100% and the system enters a loss scenario. When this happens, losses are absorbed in a strict order.

First, current period premiums are used to pay claims. If claims exceed those premiums, losses next draw down retained capital and accumulated reserves on Re’s balance sheet. This is the first-loss layer that grows during profitable years. If those reserves are fully depleted, losses then reach reUSDe, the junior tranche. Only after the junior tranche is exhausted would losses reach reUSD, the senior tranche.

Tail Risk Framing

Because the structure contains multiple layers, a senior capital impairment requires an extreme sequence of events. Premium income would first need to be overwhelmed by claims. Retained capital would then need to be fully depleted. The junior tranche would also need to be exhausted. Only after all three layers are consumed would the senior tranche be reached.

To put it in perspective: If the combined ratio were to exceed roughly 135%, the probability of losses reaching the senior tranche is approximately 0.03%. In practical terms, this would mean an unprecedented loss scenario: all lower protection layers have already been fully exhausted and reUSD principal protection is triggered.

For this to happen, losses would need to reach levels far beyond any insurance event ever recorded. (Note: This figure does not represent a guarantee. It reflects modeled outcomes based on diversified underwriting exposure and historical volatility patterns within the underlying insurance lines.)

The goal is not to eliminate risk. It is to structure it clearly, define how losses flow, and align return with position in the capital stack.

Why reUSDe Earns More

The yield difference between reUSDe and reUSD reflects where each sits in the capital structure. reUSDe is positioned closer to underwriting performance.

In most years, underwriting remains profitable. Premiums exceed claims, retained capital grows, and the junior tranche earns yield from the underlying insurance activity.

Because it sits closer to underwriting results, reUSDe carries more exposure to fluctuations in performance and earns a higher return.

Why reUSD Is Designed to Be Remote

As the senior tranche, reUSD is designed to sit further away from routine underwriting variability and benefits from several layers of protection: premium income absorbs the first portion of losses, then retained capital from prior profitable years forms a growing first-loss buffer, followed by the junior tranche.

As retained capital compounds over time this first-loss layer becomes thicker. That dynamic increases the distance between normal underwriting outcomes and the senior tranche.